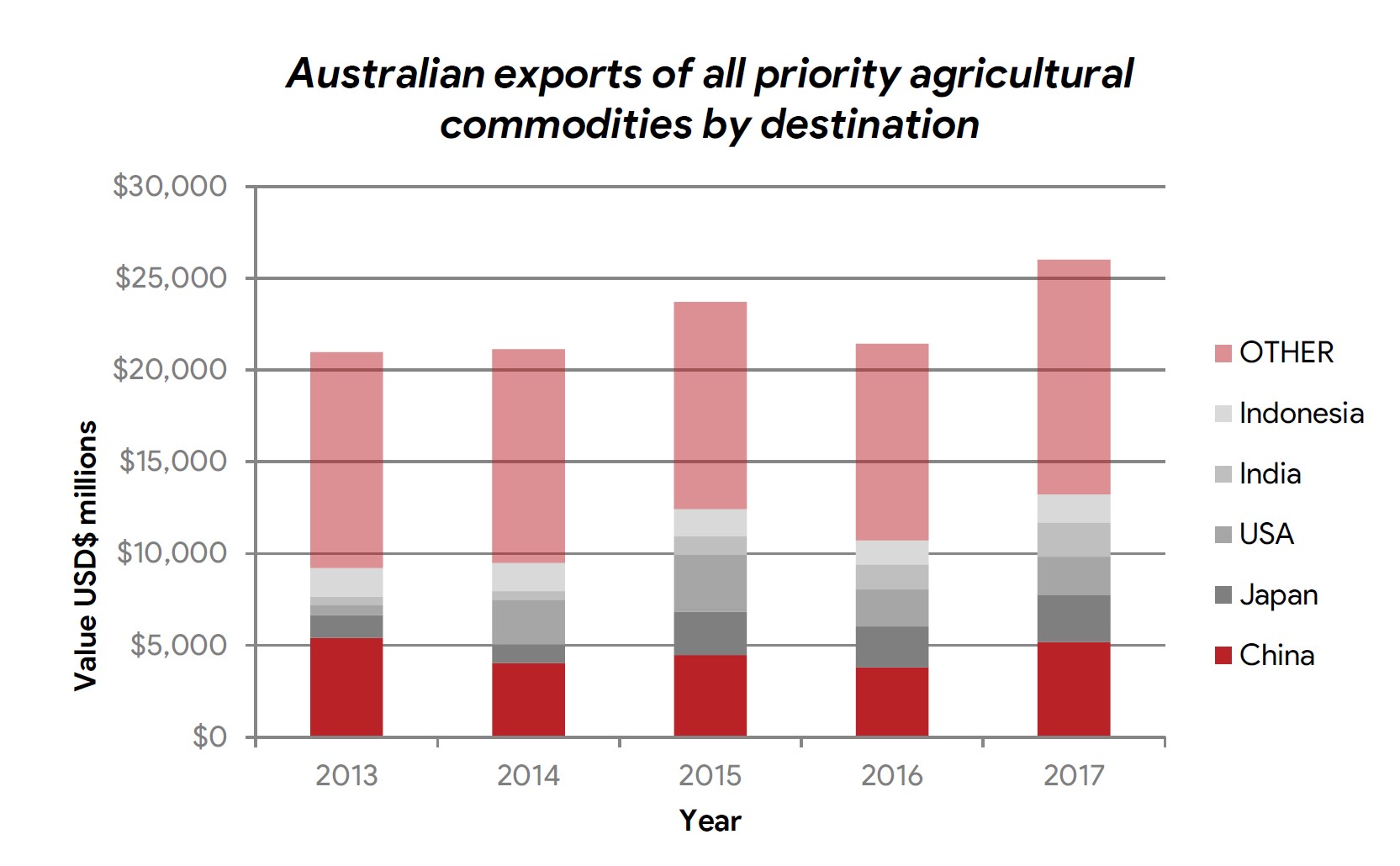

A comprehensive AgriFutures Australia-funded report released today gives policy makers, industry peak bodies and primary producers a roadmap as to how a less predictable trading environment may impact export markets.

AgriFutures Australia Managing Director, John Harvey said the ITS Global analysis, Bilateral trade wars, Understanding the implications for Australian agriculture, gives the industry a firm footing for policy creation.

“This robust analysis gives Australian exporters the knowledge they need to take a leadership role in attempting to restore stability for agricultural commodities in the current global trading environment,” said Mr Harvey.

“The findings show that unilateral moves by the Trump Administration to renegotiate existing trade agreements have threatened World Trade Organisation (WTO) principles of a rules-based trading system, creating uncertainty for Australian agriculture.”

The report identified a wide range of risks and opportunities for Australia’s agricultural interests arising from the current trade wars, finding some Australian products are likely to fare better than others.

AgriFutures Australia Senior Manager, Business Development, Jen Medway agreed that while some industries will prosper and others may feel the pressure from these trade wars, understanding the potential impact is fundamental to creating stability in an unsettled trade environment.

“Australia’s dairy industry is one industry that could potentially benefit from trade opportunities with China on the back of additional tariffs imposed on US dairy products.

“On the flip side, a prospective US–Japan free trade agreement (FTA) could negatively impact the dairy industry as US producers disadvantaged in the Chinese market could gain improved access to Japan.

“For the Australian wool industry, the bilateral trade wars may not have a noticeable impact, despite China implementing retaliatory tariffs on some US wool products. The relatively small size of the US wool export market to Asia will buffer any significant uncertainty for Australian wool exporters as a result of the increased tariffs,” said Ms Medway.

This is similar for Australian sheep and goat meat exports, primarily lamb, where the aftermath of the trade wars are expected to be minimal. These products have not been the focus of additional tariff actions, however a US-United Kingdom (UK) FTA (following the UK’s exit from the European Union) would have a negative impact on some Australian markets.

“The UK is a leading sheepmeat exporter and the US is Australia’s most important market, any improvement in access for UK product into the US would be damaging to Australia’s export interests,” said Ms Medway.

Another area we may see increased competition is in Australia’s fresh, chilled and frozen beef exports due to risks identified in Australia’s two biggest beef export markets – Japan and the US.

“The US is increasingly eager to expand their export reach of beef products into Japan, with the US having very limited access to China and the EU due to a ban on hormone growth promotants. With the US and Japan edging closer to negotiating a bilateral FTA, Australian beef exports to Japan may suffer,” said Ms Medway.

Mr Harvey acknowledges the importance of the report findings, noting they are critical to putting rigor around our understanding of the top line impacts for agriculture products as a result of the trade wars.

“It will inform Australian industry input on how best to ameliorate the detrimental side effects of current and possible future trade measures,” Mr Harvey said.

Mr Harvey added that the take-away message from the research is that trade wars breed uncertainty. Uncertainty is bad for business and leaves agricultural producers, traders and buyers struggling to manage a shifting policy landscape.

“The longer this period of uncertainty lasts, the more commercial decisions will need to be made by Australia’s agricultural stakeholders facing the prospect of sudden and unpredictable policy changes at the global level,” Mr Harvey said.

As a medium-sized, open economy dependent on trade to underpin economic growth, Australia benefits significantly from the confidence and predictability inspired by the smooth operation of the international trade regime.